Buying a car is expensive. The monthly payment often feels like a punch to the gut until you sit down with a calculator. But the real cost isn't just the sticker price; it's the interest rate. A difference of just one percent over five years can mean thousands of pounds or dollars extra in your pocket-or out of it. That’s why choosing the right lender matters more than picking the right color.

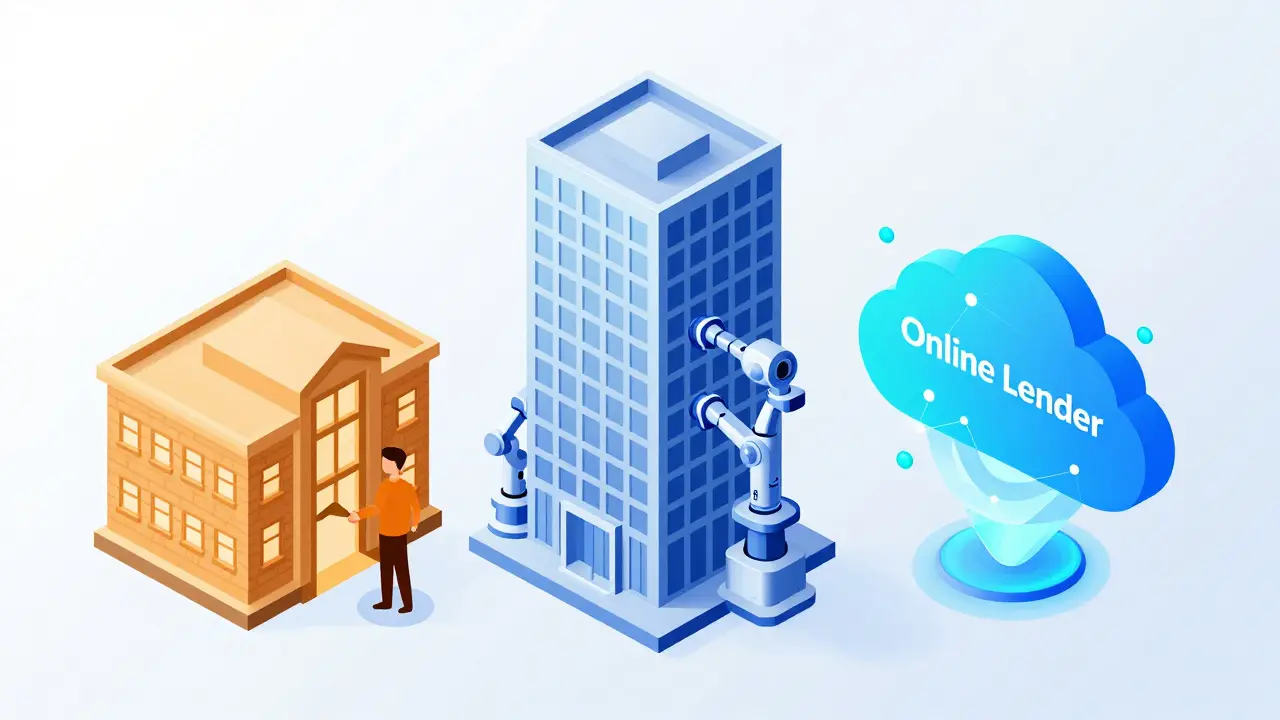

You have options. Big banks promise speed. Credit unions promise lower rates. Online lenders promise convenience. Dealerships promise ease. But which one actually saves you money? Let’s break down who offers the best auto financing in 2026, looking at hard numbers, hidden fees, and what happens when things go wrong.

Credit Unions: The Rate Kings

If your only goal is the lowest possible interest rate, start here. Credit unions are not-for-profit organizations owned by their members. Because they don’t need to generate profits for shareholders, they pass those savings back to you in the form of lower APRs (Annual Percentage Rates).

In 2026, the average APR for a new car loan from a credit union hovers around 6.5% for borrowers with excellent credit (720+ FICO score). Compare that to the national average for big banks, which sits closer to 8-9%. For used cars, the gap widens even further. While banks might charge 10-12% on a three-year-old vehicle, many credit unions offer rates under 7%.

The catch? Membership. You usually need to join before you borrow. This might mean living in a certain area, working for a specific employer, or belonging to a particular organization. However, many large credit unions like Navy Federal or Alliant have opened their doors to anyone willing to pay a small membership fee (often $5-$10) or make a small donation to a partner charity.

Is it worth joining a credit union just for a car loan?

Yes, if you plan to keep the account open. Even if you only use them for one loan, the savings on interest usually outweigh the $5-$10 membership fee. Plus, you get access to checking and savings accounts with higher yields and fewer fees than traditional banks.

Big National Banks: Speed and Convenience

Banks like Chase, Wells Fargo, Bank of America, and Citibank dominate the auto lending space because of their sheer size. They have massive apps, physical branches everywhere, and automated systems that can approve you in minutes.

Why choose a big bank? Relationships matter. If you already have a mortgage, checking account, or direct deposit set up with Chase, for example, they may offer you a "relationship discount." This could shave 0.25% to 0.5% off your base rate. It’s not as dramatic as a credit union’s spread, but it adds up.

However, be wary of the fine print. Big banks are notorious for origination fees-upfront charges just for processing the loan. These can range from $200 to $500. Always ask for the "out-the-door" cost, including all fees, before signing. Also, their customer service can feel robotic. When you call about a billing error, you’re likely to spend an hour on hold talking to AI bots before reaching a human.

Online Lenders: The Middle Ground

Companies like LightStream, SoFi, and Capital One Auto Finance operate entirely online. They’ve stripped away the branch overhead, allowing them to compete aggressively on both rate and user experience.

LightStream, owned by Truist, consistently ranks high for low rates among non-credit-union lenders. They often match or beat credit union rates for top-tier borrowers. Their application process is sleek, digital, and fast. You can lock in a rate within 24 hours.

SoFi focuses heavily on the tech-savvy borrower. They offer features like autopay discounts (0.25% off if you set up automatic payments) and no prepayment penalties. This flexibility is huge if you plan to pay off the loan early to save on interest.

The downside? Limited face-to-face support. If you have complex financial situations-like self-employment income or recent bankruptcy-online algorithms might reject you instantly. A human loan officer at a local bank or credit union might look at the whole picture and say yes.

Dealership Financing: The Trap and The Trick

Most people buy cars through dealerships. It’s convenient. You walk in, pick a car, and leave with keys. But dealership financing is rarely the cheapest option.

Dealers make money on two things: the car itself and the loan. They act as middlemen, shopping your application around to various wholesale lenders (like Ally, Toyota Financial Services, or Ford Credit) to find the highest rate they can justify for your credit profile. This is called "markup." They might secure you a 6% rate from the lender but charge you 8%, keeping the 2% difference as profit.

Here’s the trick: Get pre-approved by a bank or credit union *before* you visit the dealer. Walk in with a printed letter stating your approved rate. Use this as leverage. Tell the finance manager, "I’m getting 6.5% elsewhere. Can you beat it?" Often, they will. If they can’t, use your pre-approved loan. You still have to go through the dealer’s paperwork, but you control the interest rate.

| Lender Type | Avg. APR (New Car) | Speed | Customer Service | Best For |

|---|---|---|---|---|

| Credit Union | 6.5% | Medium (1-3 days) | High (Local/Human) | Lowest Rates |

| Big Bank | 8.5% | Fast (Same day) | Low (Automated) | Existing Customers |

| Online Lender | 7.2% | Very Fast (Hours) | Medium (Chat/Email) | Tech-Savvy Borrowers |

| Dealership | 9.5%+ | Instant | Variable | Convenience/Subsidized Offers |

How to Lower Your Rate: Actionable Tips

Your credit score is the biggest lever you have. In 2026, lenders are using more sophisticated models that look beyond just the FICO number. They check your debt-to-income ratio (DTI), recent credit inquiries, and even rental payment history if reported.

- Pay down existing debt: Reducing your credit card balances lowers your DTI. Aim for below 36%.

- Check your report: Pull your free credit report from AnnualCreditReport.com. Dispute any errors immediately. A single incorrect late payment can drop your score by 50 points.

- Shop within 14 days: Multiple hard inquiries for auto loans within a short window count as a single inquiry on your credit report. This protects your score while you compare rates.

- Put more down: A larger down payment reduces the loan amount and the lender’s risk. Try to put down at least 20% for new cars and 10% for used ones.

- Shorten the term: A 36-month loan has a higher monthly payment but a much lower total interest cost than a 72-month loan. Avoid long terms unless absolutely necessary.

Red Flags to Watch For

Not all loans are created equal. Some contain traps that can cost you dearly later.

Prepayment Penalties: Some lenders charge a fee if you pay off the loan early. This locks you into paying interest even if you sell the car or get windfall cash. Always choose a loan with "no prepayment penalty."

Negative Equity Roll-Overs: If you owe more on your current car than it’s worth, some dealers will roll that debt into your new loan. This creates a massive loan burden from day one. Refuse this. Sell the old car privately or trade it in elsewhere.

Gap Insurance Upsells: Gap insurance covers the difference between what you owe and what the car is worth if it’s totaled. It’s useful, but dealers often mark up the price by 100-200%. You can usually buy this directly from your auto insurer for a fraction of the cost.

Making the Final Decision

There is no single "best" bank for everyone. It depends on your priorities.

If you want the absolute lowest rate and don’t mind jumping through hoops to join, go with a Credit Union is a member-owned financial cooperative that provides banking services to its members.. Examples include Navy Federal Credit Union (for military families) or Alliant Credit Union (open to most Americans via membership drive).

If you value speed and already have a relationship with a major bank, check if they offer a loyalty discount. Chase Auto Finance and Wells Fargo Auto are solid choices for existing customers.

If you prefer a digital-first experience with competitive rates, look at LightStream or SoFi. They offer transparency and ease of use that traditional institutions struggle to match.

Whatever you choose, never sign a contract without reading every line. Ask for the APR, the monthly payment, the total interest cost, and any fees. Write them down. Compare them side-by-side. The few hours you spend researching now will save you thousands over the life of the loan.

What credit score do I need for the best auto loan rates?

To qualify for the best rates (sub-7%), you typically need a FICO score of 720 or higher. Scores between 660-719 will still get you good rates, but slightly higher. Below 620, options become limited and rates increase significantly.

Can I negotiate the interest rate at the dealership?

Yes, but it’s harder than negotiating the car price. Bring a pre-approval letter from another lender. Use it as a benchmark. If the dealer can’t beat it, use your own loan. Never accept a rate without knowing what other lenders are offering.

Are there any fees associated with auto loans?

Common fees include origination fees ($200-$500), documentation fees ($100-$400), and title fees ($50-$100). Credit unions often waive origination fees. Always ask for a breakdown of all fees before signing.

Should I refinance my auto loan?

Refinancing makes sense if interest rates have dropped significantly since you took out the original loan, or if your credit score has improved. Check if your current loan has a prepayment penalty. If not, refinancing can lower your monthly payment or shorten the loan term.

What is the difference between APR and Interest Rate?

The interest rate is the cost of borrowing the principal amount. The APR (Annual Percentage Rate) includes the interest rate plus any fees or costs associated with the loan. Always compare APRs to get the true cost of the loan.