When you trade in a car that you still owe more on than it’s worth, you’re carrying negative equity into your next loan. It sounds like a simple fix - just add the leftover balance to your new car payment - but it’s one of the most common financial traps in auto financing. And if you don’t understand how it works, you could end up deeper in debt than when you started.

What Is Negative Equity?

Negative equity, also called being "upside down" on a loan, happens when the amount you owe on your car is higher than what the car is worth. For example, if you owe £12,000 on your current car but the dealer offers you £9,500 for it, you’ve got £2,500 in negative equity. That gap doesn’t vanish when you buy a new car. Instead, it gets added to the price of your next vehicle.

This isn’t rare. According to data from the UK’s Finance & Leasing Association, over 22% of used car buyers in 2025 carried over negative equity from previous loans. The average amount rolled over? £3,200. That’s not pocket change. That’s a financial anchor.

How Rolling Negative Equity Works

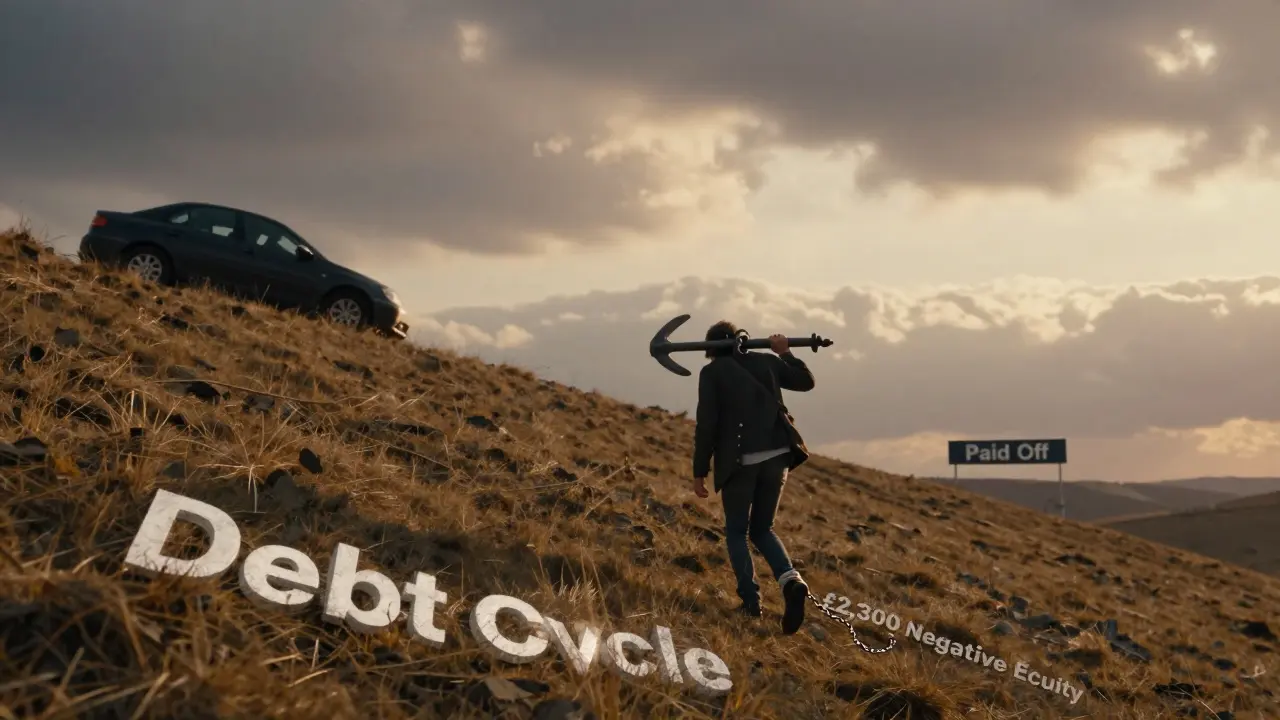

Here’s how it plays out in real life:

- You owe £11,000 on your 2021 Ford Focus.

- You trade it in. The dealer values it at £8,700.

- You pick a new 2025 Hyundai Kona priced at £23,000.

- The dealer adds your £2,300 deficit to the new loan.

- Your new loan total? £25,300.

You didn’t just buy a £23,000 car. You bought a £25,300 car - and you didn’t even get a discount for the trade-in. That £2,300 becomes part of your monthly payment, your interest, and your long-term debt.

And here’s the kicker: you’re now financing a car that’s likely worth less than what you paid for it the moment you drive it off the lot. Depreciation hits fast. A new car loses 15-20% of its value in the first year. If you roll over debt, you’re starting behind the eight ball.

Why Dealers Encourage It

Dealers don’t tell you this, but rolling over negative equity is profitable for them. Here’s why:

- It increases the loan amount - which means higher commissions for the finance manager.

- Longer loan terms (72 or 84 months) become easier to sell when the monthly payment looks manageable.

- You’re less likely to walk away if you’ve already been told, "We can fix it in the financing."

Some dealers even offer "zero down payment" deals on new cars - but only if you roll over your old loan. That sounds convenient. It’s not. You’re trading short-term ease for long-term pain.

The Hidden Costs

Rolling negative equity doesn’t just add dollars to your loan. It adds risk.

More interest over time - The extra £2,300 you rolled over doesn’t just sit there. It accrues interest. At 7.5% APR over 6 years, that £2,300 becomes £2,900 in total payments. You’re paying £600 just to carry debt from a car you already owned.

Longer loan terms - To keep payments low, lenders push you toward 72- or 84-month loans. That means you’ll be paying for a car for seven years. Most cars last five to six years before major repairs start. You could be paying off a car that’s falling apart.

Lower resale value - If you need to sell or trade in again before the loan is paid off, you’ll likely be upside down again. You’re stuck in a cycle. And if your car gets totaled or stolen early? You’ll owe the full loan balance - even if the insurance only pays out what the car was worth.

What Happens If You Can’t Keep Up?

Life changes. You lose your job. Your car breaks down. Your income drops. If you’re carrying rolled-over debt, you’re one bad month away from repossession.

Repossession doesn’t just hurt your credit. It leaves you with a black mark for seven years and still owes the remaining balance. Say your car is repossessed after you’ve paid £8,000 on a £25,000 loan. The lender sells it at auction for £14,000. You still owe £3,000 - plus repossession fees. That’s £3,000 you didn’t even get to drive.

According to UK finance watchdogs, repossession claims involving rolled-over equity rose 18% between 2023 and 2025. The most common trigger? People who rolled over £2,000 or more.

How to Avoid the Trap

You don’t have to roll over negative equity. Here’s what actually works:

- Wait until you’re not upside down. Keep driving your current car. Pay down the loan. Even £100 extra a month cuts your negative equity fast.

- Save for a bigger down payment. If you can put down £3,000-£5,000 on a new car, you’re less likely to go upside down again.

- Buy used. A 2-3 year old car with low mileage often costs 30% less than new - and depreciates slower.

- Get a shorter loan term. 48 months instead of 72. It means higher payments, but you’ll own the car before it starts costing you in repairs.

- Use a loan calculator. Plug in the numbers before signing anything. See how much you’ll really pay over time.

One woman in Bristol paid off her £4,000 deficit over 14 months by driving her old car, cutting cable, and putting £300 a month toward her loan. She then bought a 2023 Toyota Corolla with no trade-in - and paid cash for the down payment. She’s now debt-free on her car. No monthly payments. No stress.

What If You Already Rolled It Over?

If you’re already in this situation, don’t panic - but don’t ignore it either.

- Check your loan balance monthly. Know exactly how much you owe.

- Make extra payments. Even £50 extra each month reduces interest and shortens your term.

- Refinance if rates drop. A lower APR can save you hundreds.

- Don’t trade in again until you’re even or in positive equity.

There’s no magic fix. But every pound you pay extra now is one pound less you’ll owe later.

The Bigger Picture

Car loans aren’t just about transportation. They’re about financial health. Rolling negative equity into a new loan feels like a shortcut - but it’s really a detour that leads straight to financial stress.

The UK’s Financial Conduct Authority has flagged this practice as a growing risk. They’re not banning it. But they’re warning lenders to be clearer about the long-term impact. That means you need to be smarter.

You don’t need the newest car. You need a car you can afford - without dragging debt from your past into your future.

Is rolling negative equity into a new loan illegal?

No, it’s not illegal. Dealers and lenders are allowed to roll over negative equity. But they’re required under UK consumer credit laws to clearly explain the total cost of the loan, including any transferred balances. If they hide the added amount or misrepresent the monthly payment, that’s a violation.

Can I roll negative equity into a lease?

Yes - and it’s even riskier. Leases have strict mileage limits and end-of-term fees. Rolling over debt means you’re paying for a car you’ll never own, on top of debt from a car you already gave up. If you end the lease early, you’ll owe the full remaining balance. Most people who do this end up paying thousands more than they planned.

How do I find out how much negative equity I have?

Check your latest loan statement for the payoff amount. Then check your car’s current market value using a trusted source like Autotrader.co.uk or Glass’s Guide. Subtract the trade-in value from what you owe. If the result is positive, that’s your negative equity.

Does insurance cover negative equity?

Standard car insurance does not. If your car is totaled, you’ll only get the current market value - not what you owe. Gap insurance covers the difference between what you owe and what your car is worth. It’s worth considering if you have negative equity - but it doesn’t fix the root problem.

What’s a better alternative to rolling over debt?

Keep your current car until you’re no longer upside down. Use that time to build a down payment fund. Then buy a reliable used car with cash or a short-term loan. You’ll save on interest, avoid depreciation traps, and end up with more money in your pocket.

If you’re thinking about trading in your car, pause. Run the numbers. Ask for a breakdown of the loan. Don’t let convenience cost you more than you can afford.

Comments

Aimee Quenneville

I swear, dealers are basically con artists with spreadsheets. They smile, hand you a pen, and say "we can fix it" like it's a magic spell. But nope - you just signed a 7-year loan for a car that's already worth less than what you owe. And now you're stuck paying for a ghost.

My cousin did this. Bought a "new" SUV, rolled over $8k from her old junker. Two years later, the transmission died. Insurance paid $14k. She owed $29k. Still owes $15k. On a car she never owned.

Don't be her.

March 19, 2026 at 20:51

TIARA SUKMA UTAMA

I did this. Got a new car. Rolled over $3k. Thought I was being smart. Turns out I was just dumb. Now I'm paying $500 a month for 7 years. I hate my life.

March 20, 2026 at 19:24

Cynthia Lamont

OMG this is so true. I read this and immediately thought of my ex who rolled over $6k. He got a "new" truck. It was a 2025 model. He drove it 6 months. Then lost his job. Repo man came. Insurance paid $18k. He owed $31k.

He still owes $13k. And now he's on food stamps. And still drives a 2014 Corolla he bought with cash.

Lesson? Don't be a sucker. Buy used. Pay cash. Or don't buy at all.

March 20, 2026 at 20:32

Liam Hesmondhalgh

This is why America is broke. People think cars are investments. They're not. They're liabilities. And dealers know it. They're not selling cars. They're selling debt. And you're buying it like it's a lottery ticket.

UK’s FCA is right. But they’re too polite. They should ban this practice. Like, outright. No more rolling. Period.

March 22, 2026 at 13:58

Jennifer Kaiser

There's a deeper layer here. It's not just about money. It's about identity. We’ve been sold the myth that a new car = success. That’s why people do this. Not because they need it. But because they fear being seen as "less than."

That £3,200 isn’t just debt. It’s a tax on your self-worth. And it’s collected by people who know exactly how to exploit that fear.

Real freedom isn’t driving a new car. It’s driving an old one without panic. It’s sleeping at night knowing you didn’t trade your future for a shiny badge.

The woman in Bristol? She didn’t just save money. She reclaimed her autonomy. That’s the real win.

March 22, 2026 at 17:22

Dmitriy Fedoseff

As someone who grew up in a family where cars were repaired, not replaced, I can say this: the moment we started treating vehicles as status symbols instead of tools, we lost something vital.

Canada’s auto culture is slowly adopting this American trap. But we don’t have to. We have winters, we have public transit, we have logic.

Why buy a new car when a 2019 Honda Civic can last another 100,000 km? Why pay interest on a depreciation curve that’s steeper than a ski slope?

It’s not about being cheap. It’s about being intentional. And intentionality is the rarest currency these days.

March 23, 2026 at 18:43

Morgan ODonnell

I used to think rolling over debt was normal. Then I met a mechanic who said, "If you can’t afford the car without the old debt, you can’t afford the car."

That stuck with me. I kept my 2017 Civic. Paid off the loan. Then bought a 2020 Hyundai with cash. No loan. No stress.

People think saving is hard. But it’s just choosing. And choosing is the only thing that matters.

March 25, 2026 at 04:07

Kirk Doherty

I’m not against cars. I’m against debt. And this is just debt dressed up like a deal.

March 25, 2026 at 16:35

Jasmine Oey

I mean… like… ugh. I just got a new car last month and I rolled over $4k. I KNOW I shouldn’t have. But the dealer said I’d be "way better off" and gave me free coffee and a gift card. I was like… ok fine.

Now I’m crying into my avocado toast because my payment is $620. I’m not even rich. I just wanted to feel like I made it.

Why do I always do this? Why am I so weak?

Can someone hug me? Or just tell me I’m not alone?

March 26, 2026 at 05:30

Meghan O'Connor

This article is correct. But it’s also incredibly naive. You think people don’t know this? They do. They just don’t care. Because they’ve been conditioned to believe that debt = progress.

And the fact that you’re even surprised by this? That’s the problem. This isn’t a trap. It’s the system. And the system wins. Always.

March 27, 2026 at 22:11

James Winter

Why are we even talking about this? In Canada we don’t do this. We buy used. We fix them. We drive them till they die.

This is why Americans are broke. You want a new car? Save. Wait. Work. Don’t let some finance guy in a polo shirt convince you that debt is a lifestyle.

March 29, 2026 at 05:31

Marissa Martin

I read this and felt so guilty. I rolled over $5k. I’m still paying it. I don’t even like this car. But I’m too scared to sell it. I’m just… stuck. And I hate that I let this happen.

March 29, 2026 at 16:19